.svg)

%20(1).png)

Table of contents

Table of contents

.svg)

⚖️ Disclaimer: This guide is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Givebutter Wallet is a financial home base, not an investment account. Investment performance is never guaranteed, and rates and regulations vary by state and provider. Consult a licensed financial advisor, tax professional, or attorney for guidance tailored to your nonprofit.

Most nonprofits work hard to raise every dollar, but many don't realize those dollars could be working just as hard in return. If your reserves are sitting in a low-yield checking account, inflation may quietly be eating away at their value over time.

Nonprofit investing isn't just for large foundations or finance-savvy teams. It's a practical, responsible way to stretch your mission further—and it's more accessible than you might think.

In this guide, we'll walk through the prerequisites for nonprofit investing, common investment options, and how to put your funds to work responsibly.

Key takeaways

- Yes, nonprofits can invest 💰 There are no legal restrictions on investing nonprofit funds, and it's part of responsible stewardship.

- Reserves first 🏦 Aim for 3–6 months of operating expenses in liquid reserves before exploring endowments.

- Inflation erodes value 📉 Idle funds in a checking account lose value each year, while investing helps preserve purchasing power.

- Governance matters ⚖️ Clear policies and legal compliance protect your organization and your donors.

- Fundraising is the foundation 🧈 Strong, predictable revenue makes investing possible.

- Start earning now 💳 Even if you're not ready to invest, Givebutter Wallet lets your funds earn APY rewards as soon as they settle—no reserves required.

Can nonprofits invest money?

Yes, nonprofits can invest money. There are no legal restrictions on investing nonprofit funds, and it's a responsible way to manage reserves. Investing can help organizations grow funds, build long-term assets, and increase financial sustainability.

How much should you have in reserves before investing?

Aim to build enough reserves so you can invest confidently without worrying about day-to-day operating costs. A common benchmark is to keep at least three to six months of operating expenses in reserve.

How much you need within that range should be based on several factors: how stable your revenue is, how established your organization is, and how much financial risk you can handle.

For example, an established nonprofit with consistent funding may need a smaller buffer than a newer organization that relies on grants.

How to calculate your reserve target

To calculate your reserve target, first determine your monthly operating expenses using this formula:

Total annual operating budget ÷ 12 = one month of operating expenses

For example, a nonprofit with a $600K annual budget has about $50K in monthly expenses.

Once you have this figure, you can work out your reserve target:

Reserve target = one month of operating expenses x 3 (or 6)

For this example organization, the reserve target is $150K–$300K.

💡 Pro tip: Keep reserve funds liquid and accessible, not locked into long-term investments. Maintaining your reserve target ensures you have a buffer for unexpected expenses or reduced income.

Are you ready to invest?

Nonprofit investing should be grounded in practical, strategic thinking. Before you get started, ask yourself these questions:

- Do you have three to six months of reserves available?

- Do you have predictable fundraising and revenue streams?

- Does your board have the financial literacy to oversee investments?

- Are you comfortable with investing as a long-term commitment?

If you answered yes to all of the above, you're in a strong position to begin investing.

Not quite there yet? That's completely normal, and this guide can still help you build toward it. Focus on one action at a time, like financial training for board members or steadily growing your reserves.

Investing for small nonprofits: How to put your reserves to work

Stocks, bonds, and crypto can be appealing, but they often come with significant volatility and risk. For nonprofit investing, low-risk, liquid opportunities are the priority.

Some organizations explore automated or robo-investing platforms, but these are generally better suited to larger nonprofits with more sophisticated investment needs—most small organizations are better served by the low-risk options below. Here are some of the best options for small organizations.

*Rates as of March 2026. Always check your provider for the most up-to-date information.

Treasury bills 🏛️

Treasury bills are short-term U.S. government debt securities. They're popular with nonprofits because they're lower risk, have low minimum investment requirements, and offer a fixed rate of return. They're also easy to purchase through TreasuryDirect.

📈 Typical rates: Around 3.3–3.7% (March 2026)

⭐️ Best for: Organizations willing to trade a bit of liquidity for slightly higher, government-backed returns

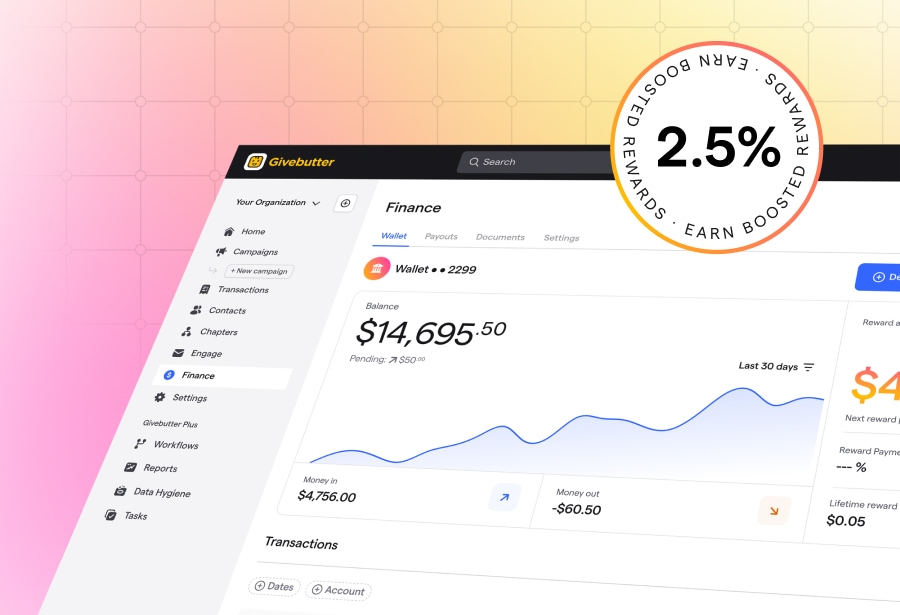

Givebutter Wallet 💳

Givebutter Wallet is a built-in financial home base that helps nonprofits put idle funds to work while earning APY rewards. Wallet deposits are eligible for pass-through FDIC insurance up to $250K through Fifth Third Bank N.A., Member FDIC.

Let your money grow while you fundraise

High-yield savings accounts 💰

High-yield savings accounts offer higher interest rates than traditional checking accounts while remaining accessible. These accounts are FDIC-insured up to $250K, which is suitable for many nonprofits, but may introduce practical considerations for organizations with larger reserve funds.

📈 Typical rates: Between 2.75–3.75% (March 2026)

⭐️ Best for: Nonprofits that want the most liquidity and prefer a simple approach to investing

Money market accounts 💲

Money market accounts are a type of bank deposit account that may offer higher rates than standard savings accounts, though they're often comparable to high-yield savings accounts. Like high-yield savings accounts, they're FDIC-insured up to $250K when held at an FDIC-insured bank.

They often come with practical tradeoffs like minimum balance requirements or limits on monthly withdrawals, which introduces a small amount of friction compared to a standard savings account.

📈 Typical rates: Between 2.75–4.00% (March 2026)

⭐️ Best for: Nonprofits that want the potential for higher yields and are comfortable meeting minimum balance requirements

Certificates of deposit (CDs) 💸

Certificates of deposit (CDs) are low-risk savings products that offer a fixed interest rate over a set term. They're designed for longer-term investing and may include penalties for early withdrawal. Like high-yield savings accounts, CDs are FDIC-insured.

Many nonprofits use a "CD laddering" strategy: instead of putting all your reserves into one CD, you spread funds across several with staggered end dates (one maturing in 1 year, another in 2, another in 3). As each one matures, you can reinvest or access the funds. You get the higher rates of longer-term CDs without locking everything up at once.

📈 Typical rates: Around 3.8–4.5% (March 2026)

⭐️ Best for: Nonprofits that want to balance liquidity with higher, fixed returns over time

How to invest nonprofit funds responsibly

Strong governance and financial stewardship protect your organization, your donors, and your board. Here's what to know before you begin investing nonprofit funds.

Step 1: Understand your legal obligations ⚖️

Most nonprofit organizations in the U.S. must comply with the Uniform Prudent Management of Institutional Funds Act (UPMIFA) when investing. The key principles are to invest prudently, preserve purchasing power, and honor donor intent.

In practice, this means avoiding unnecessarily risky investments, keeping up with inflation, and making sure restricted funds are used the way donors intended.

💡 Pro tip: Legal requirements vary by state, so review your state's specific requirements regarding nonprofit investing.

Step 2: Build your nonprofit investment policy 📋

Investment decisions should be strategic and aligned with your organization's goals and appetite for risk. A clear nonprofit investment policy sets guardrails that inform what you will or won't invest in, so staff can make consistent, informed decisions.

Your policy should include:

- Asset allocation

- Risk tolerance

- Spending rules

- Decision-making authority

- Review schedule

Step 3: Know when to bring in a professional 🤝

Staff can often manage routine investing decisions, but when you reach a certain level, professional guidance becomes more valuable. Many nonprofits work with a Registered Investment Advisor (RIA), especially once reserves reach $500K–$1M.

A strong advisor relationship is key to successful investing operations. To find the right partner, ask:

- What is your experience working with nonprofits similar to ours?

- How will you reflect our mission and goals within the investing portfolio?

- What is your approach to risk management?

The answers to these questions will help you determine whether an advisor aligns with your organization's priorities.

💡 Pro tip: Smaller nonprofits may benefit from working with a community foundation as a more accessible alternative to an RIA.

Grow your financial reserves with Givebutter

Investing is a long game, and you're now equipped to play it well. The next step is making sure the revenue coming in is just as strong as the strategy you're building.

Consistent fundraising is what makes investing possible. Predictable income builds healthy reserves, and healthy reserves create the foundation for long-term financial growth.

Sign up for Givebutter today to start fundraising smarter and put your nonprofit's investing strategy into action.

FAQs about investing for nonprofit organizations

Are nonprofits allowed to invest money?

Yes, nonprofits can invest money, and it's often a responsible way to manage reserves, as long as you maintain sufficient funds for operating expenses.

Can nonprofits invest restricted funds?

Yes, but only in accordance with donor restrictions and your investment policy. Proper documentation is essential to ensure compliance and transparency. Typically, losses are applied to unrestricted funds first to protect restricted assets.

Where should a nonprofit open an investment account?

Nonprofits have several options for opening an investment account. Brokerage firms like Fidelity or Vanguard offer low minimums. Community foundations are often more affordable for smaller organizations and provide governance support. Nonprofit-focused RIAs are ideal for organizations with more substantial reserves.

What are the safest investment options for nonprofit reserves?

The lowest-risk investment options are those with FDIC or U.S. government backing, which include treasury bills, high-yield savings accounts, and certificates of deposit (CDs). Other options, like money market accounts, may offer higher returns but introduce slightly increased risk.

Can nonprofits earn interest on their funds?

Investment income from traditional investments like dividends, interest, and capital gains is generally tax-exempt for 501(c)(3) nonprofit organizations. However, investment income from debt-financed investments or certain partnership structures may be subject to Unrelated Business Income Tax (UBIT). Check with your tax advisor to confirm what applies to your organization.

Share this article

Subscribe

150K+ changemakers already subscribed